ABOUT INSURANCE ADVISERNET

Insurance Advisernet Australia was founded in 1996 and Insurance Advisernet New Zealand in 2006. Today we’re one of the largest and most respected general insurance businesses in Australia and New Zealand, with an ever growing network of over 250 authorised insurance advice practices.

As part of the AUB Group, an ASX-listed company, with over $4 billion in premium under influence across the AUB network, our buying power spans major insurers in Australia as well as access to major overseas insurers.

Insurance Advisernet have won the ANZIIF industry award for Authorised Representative Network of the Year since 2018 through to 2021!

ADVICE YOU CAN TRUST

Trust sits at the heart of any successful relationship. It’s the cornerstone on which Insurance Advisernet is built. For two decades Insurance Advisernet has grown through an unwavering trust from business owners across Australia and New Zealand; that we’ll always be transparent, do what we say we’ll do, and go further to understand your risk profile and ensure your insurance needs are accurately and objectively met. This trust has seen us become one of Australasia’s leading general insurance broker dealer groups by delivering the very best advice, the most efficient systems and the right insurance solutions for every individual client. It’s a trust we never take lightly or for granted. And one we look forward to sharing with you.

WHY CHOOSE INSURANCE ADVISERNET

Every year more and more businesses entrust their risk management requirements to Insurance Advisernet and enjoy considerable benefits in doing so. By choosing an authorised Insurance Advisernet representative, you will too.

The Four Pillars of Insurance Advisernet

We believe in delivering you the very best advice, the most efficient systems and the right insurance solutions, all built upon our four core business pillars: Trust, Advice, Choice & Value.

Advice

Great advice is based on great understanding and relationships. It’s why adopting a risk

management approach and assessing your unique risk profile is essential to ensuring the

right policies are always in place. It’s what sets us apart.

Trust

Trust is the cornerstone on which our business is built. It means we do what we say we’ll do. Use our expertise to put your needs first and foremost. And are always transparent about the advice we provide and why we provide it. AdviceGreat advice is based on great understanding and relationships. It’s why adopting a risk management approach and assessing your unique risk profile is essential to ensuring the right policies are always in place. It’s what sets us apart.

Value

Price is always important. But value goes much further. It’s the sum total of the depth of our

relationships, the quality of our advice, the breadth of our offering and the efficiency of our

systems – all bolstered by our unrivalled buying power as one of the leading general insurance broker dealer groups. Ultimately though, our key value to you is as your advocate in the event of a claim.

Choice

Insurance is no time for compromise. It’s vital to have access to a wide range of insurance options so, once identified, your needs can be effectively met. It’s why we have active relationships with more than 100 major insurers.

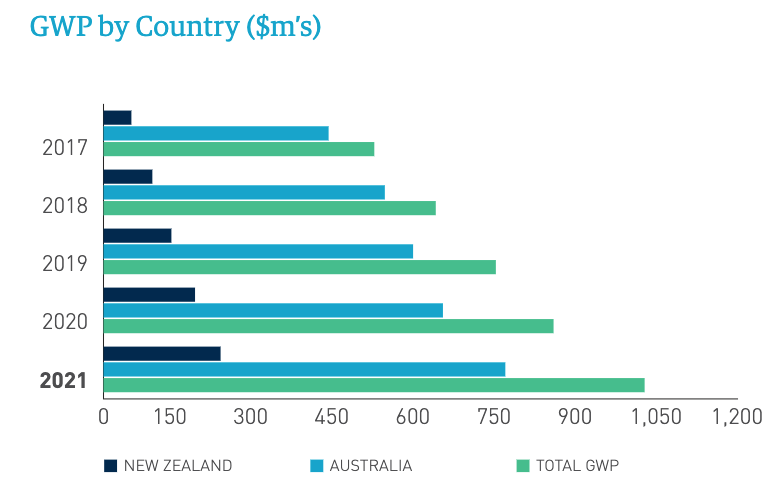

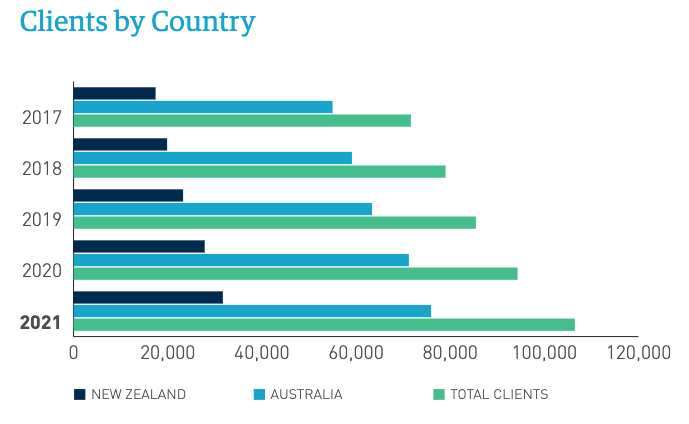

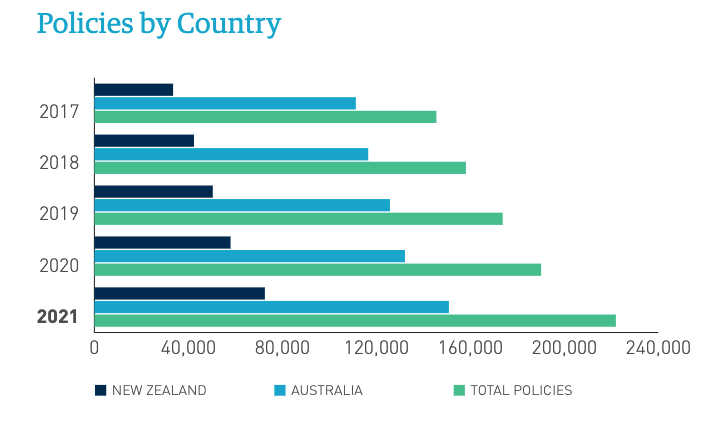

THE SUCCESS

The following graphs indicate the outstanding growth that Insurance Advisernet has achieved since inception and is a testimony to the success of the model and quality of the people within our network.

THE PURPOSE

Our vision is to provide insurance advisers with the benefits of maintaining their local presence whilst being able to tap into a national buying group for products and services needed by their customers in today’s complex business world.

Our Vision

- Be a dynamic, market leading general insurance broking dealer group Deliver superior business systems, products and services to our advisers

- Be innovative, agile and adept to remain relevant in a fast-changing insurance environment

- Attract and retain highly professional team-orientated people

- Retain our family culture with embedded values and people who ‘walk the talk’

- Encourage a superior life/family/work balance

Our Mission

- Provide our advisers with an AFSL, products and services that add superior value and become an integral part of their business

- Be an advocate to protect, enhance and grow our advice practices

- Deliver business tools that help our advisers provide quality professional advice and training

- Provide our advisers with sound business advice

- Provide our advisers with high quality new business referrals

- Above all, consult and listen to our advisers to ensure everything we do allows them to achieve their personal and business goals with Insurance Advisernet

Through this vision and mission Insurance Advisernet advisers are able to offer their customers:

- Competitively priced products

- Peace of mind in their insurance arrangements

- Access to leading Australian and international insurers

- Sincere and personalised working relationships

- More profitable, productive and safer workplaces for their staff

- Claims advocacy advice to support our clients through the claims process

CLAIMS ADVOCACY

Being there for our clients at the time of a claim is probably the most important role your Insurance Advisernet Adviser can play. At times the claims process can be long and complex, but at Insurance Advisernet we work closely with our clients and insurer partners to make this process as simple and efficient as possible for you – ensuring you are back in business or on the road sooner!

At Insurance Advisernet, your adviser is there to guide our clients through the claims process. From lodgement of the claim, monitoring progress and negotiating with our insurer partners to ensure the best possible outcome for our clients.

Ultimately our key value to you is as your advocate in the event of a claim.

Our Claims Management Philosophy

- Act fairly in the interests of our clients in the event of a claim

- Assist our clients in the claims lodgement process through to finalisation of the claim

- Assist our clients to understand overly complex policy interpretations

- Assist our clients to reduce the cost and the number of claims through effective risk

- management strategies

- Provide 24hr emergency claims assistance where required

In the Event of a Claim

- Assist our clients in lodging claims and maintain communication every step of the way

- Advocate and negotiate with insurers on behalf of our clients to ensure they receive

- their full entitlements

- Arrange for a loss assessor to be appointed

- where required

- Arrange expert consultants including legal and accounting services where needed

- Arrange access to Risk Management services to assist in prevention or mitigation against future loss

At Insurance Advisernet we also understand that not all incidents occur during normal business hours, that’s why we have established Insurance Advisernet 24/7 Emergency Claims Response. This ensures that our clients always have assistance on hand no matter what time of day. Simply give us a call on 1300 831 094.

5 STAR BEST PRACTICE

Insurance Advisernet is committed to providing our clients with advice on insurance best practice in key risk areas. Our 5 Star system provides our clients with a snapshot of how they are performing against industry best practice in respect to risk management, compliance and mitigation. The Insurance Advisernet 5 Star Survey & Report provides clients with a rating on their existing procedures as well as providing guidelines on how to upgrade to best practice. 5 Star Benchmarking is currently available for the following types of Insurance Risk:

- Property

- Cyber

- WHS

PORTAL

At Insurance Advisernet we value our relationship with our clients more than anything but sometimes we know it’s nice to be able to do things in your own time. That’s why we’ve created an easy-to-use online portal that’s available 24/7 from your mobile or desktop.

You can use it in a range of ways:

- Generate and download a confirmation of insurance certificate

- View all up-to-date insurance summaries – see what policies are in place and view summaries of cover

- Report an incident that might need a claim – get the conversation started if you think you might have a claim and provide some info to your adviser.

Access is easy, you can log in via IA’s website, your Advisers’ website or directly

from the Insurance Advisernet App.

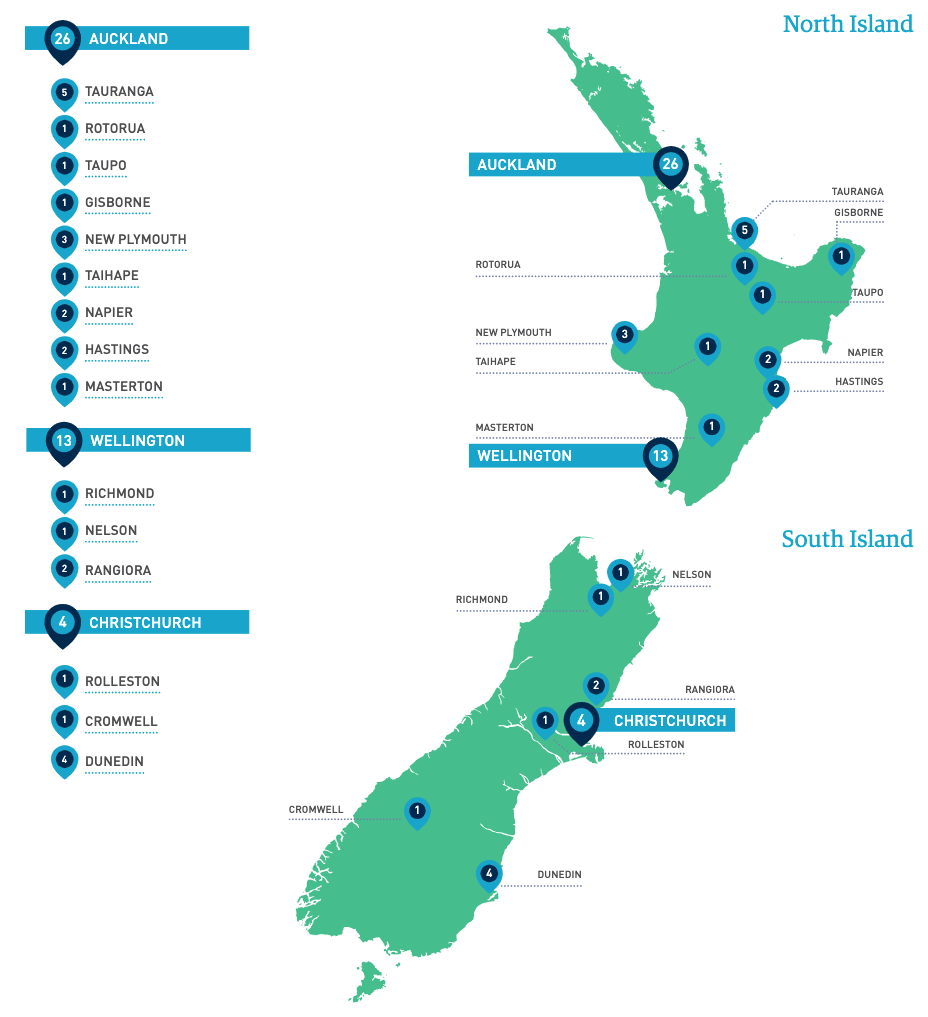

OUR NETWORK

With over 250 authorised insurance advice practices and 950 staff across Australia and New Zealand, Insurance Advisernet is one of the leading insurance dealer groups in the Southern Hemisphere. Each year we help more than 110,000 active clients and manage in excess of 220,000 policies.

OUR PARTNERS

The strength of Insurance Advisernet goes far beyond the walls of our own business. It’s also about the quality partnerships we build and nurture every day, from our ongoing relationship with the highly respected AUB Group (Austbrokers), to the insurers we choose to work with and our ongoing involvement with key industry associations.

Leading Insurers

Rather than focus on a small number of ‘favoured’ insurers, our dedicated approach has allowed us to spend many years forging relationships with the very best local and international insurance providers. The benefits of these relationships are seen every day by our clients. Insurance Advisernet advisers have access to over 100 partners to meet our clients insurance needs.

Premium Funding

For many clients and industries we understand the vital importance of

preserving day-to-day cash flow. In such situations we can help our clients spread

their insurance premium payments over time through an instalment arrangement,

arranged via our relationships with reputable insurance premium funding companies.

Industry Affiliations

As one of the leading general insurance broking groups in Australasia, Insurance

Advisernet takes a deep and active role in the insurance industry through a

variety of initiatives and affiliations.

INSURANCE ADVISERNET FOUNDATION

At Insurance Advisernet, we feel very fortunate to be part of a dynamic and successful business. The Insurance Advisernet Foundation was established as part of Insurance Advisernets ongoing commitment to our people, our clients and the wider community. The Foundation supports local Australian and New Zealand organisations that work to help change the lives of individuals, families and/or communities for the better.

Insurance Advisernet and its Foundation has contributed over $2.5 million in the last 10 years to over 30 different charities. We will continue to donate over $400,000 each year through a variety of fundraising initiatives. By working closely with our staff, advisers and our insurance underwriting partners we aim to leave a social legacy for generations to come.

OUR BOARD

IAN CARR

FOUNDER & CHAIRMAN, INSURANCE ADVISERNET AUSTRALIA & NEW ZEALAND

Ian has worked in the insurance broking industry for over 40 years. His extensive

experience includes numerous senior positions such as State Manager, General Manager and Director, Operations for a major national insurance broker in Australia. Ian founded

Insurance Advisernet in 1996 and under his stewardship Insurance Advisernet has grown

spectacularly to be one of the largest general insurance brokerages in Australia and New

Zealand. He holds an Advanced Diploma Financial Services (Broking) and is a Fellow

of NIBA, MAICD.

SHAUN STANDFIELD

MANAGING DIRECTOR, INSURANCE ADVISERNET AUSTRALIA & NEW ZEALAND

As an experienced insurance executive, Shaun boasts a proven track-record in leading

large multi-disciplined insurance sales, claims and underwriting operations and has led

significant change programs in both Australia and Asia. He holds a Bachelor of Business,

Graduate Management Qualification, Masters in Business Administration (MBA), Advanced

Diploma of Financial Services and Graduate Diploma from the Australian Institute of Company Directors.

STEPHEN ROUVRAY

NON-EXECUTIVE BOARD MEMBER

Stephen is currently a consultant to AUB Group Limited (formerly Austbrokers

Holdings Limited). He was Chief Financial Officer of Austbrokers from 2005 until his retirement in 2015. He has over 30 years’ experience in the financial services industry, covering general insurance, life insurance and investment management. He was also Company Secretary of Austbrokers from 1986 to 2015. Stephen was previously

General Manager of ING Australia Holdings from 2002 to 2005 and Company Secretary

of a number of ING subsidiaries from 1985 to 2005. Stephen joined ING’s predecessor

Mercantile Mutual as Company Secretary in 1985. From 1971 to 1984, Stephen worked in the accountancy profession where he specialised in the financial services sector concentrating on general insurance. Stephen has a Bachelor of Economics from The University of Sydney and is a Chartered Accountant.

SARAH FARMBOROUGH

FINANCIAL CONTROLLER, INSURANCE ADVISERNET

AUSTRALIA & NEW ZEALAND

Sarah brings over 15 years of high-level financial management and accounting

experience, gained in the UK, continental Europe and most recently Australia with

Insurance Advisernet. She holds an FCCA and her expertise spans financial reporting,

internal controls, consolidation, audits, process improvement, change management, budgeting and forecasting, project management, SAP, financial analysis and strategic planning.

JOHN BURKE

NON-EXECUTIVE BOARD MEMBER

John has enjoyed over 25 years in the Insurance Broking Industry in both client

facing and executive roles across Australia. His involvement with Insurance Advisernet

spans over 18 years and was previously our General Manager, Southern Region (12

years). Today, John is a Corporate Authorised Representative with Insurance Advisernet

and accordingly is well versed with our business operations.

John holds a Diploma of Insurance Broking, is an Affiliate CIP of the Australian and New

Zealand Institute of Insurance & Finance and a member of the National Insurance Brokers

Association.